The launch of flagship models by major brands helped propel global smartphone production to a QoQ increase of 7%, reaching approximately 310 million units and matching figures from the same period last year. However, production volumes for the quarter have not yet returned to pre-pandemic levels, signalling a continued lack of a clear recovery in the global consumer market.

Looking ahead to the fourth quarter, smartphone production is expected to rise nearly 7% QoQ, matching last year’s performance. This growth is expected to be fuelled by Apple’s production peak for its latest models and year-end efforts by Android brands to capture market share. However, brands are expected to maintain cautious inventory strategies to avoid increased financial strain from excessive stock.

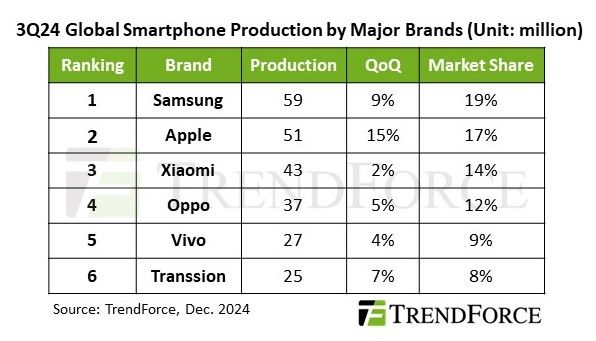

TrendForce reports that the rankings of the top six global smartphone brands remained unchanged in the third quarter, collectively commanding nearly 80% of the market. Samsung retained its leading position with a production volume of nearly 59 million units, up 9% QoQ, and a market share of 19%. Growth was driven by the mass production of its foldable series and increased stocking of mid-to-low-end A-series models for the holiday season.

Apple ranked second, with a production volume of approximately 51 million units, marking a 15% QoQ increase and a 17% market share. Apple is expected to surpass Samsung in the fourth quarter as its production peaks. However, the AI-related features of its new devices are unavailable in the Chinese market, and intense brand competition led to a year-over-year decline in sales performance in the region.

Xiaomi (including Xiaomi, Redmi, and POCO) maintained its third-place position with production reaching 43 million units, up 2% QoQ and accounting for 14% of the market. Xiaomi’s early expansion into overseas markets has become a key growth driver. Production in the fourth quarter is expected to remain steady as the brand replenishes inventory and prepares for potential Lunar New Year disruptions.

Oppo (including Oppo, OnePlus, and Realme) secured fourth place with a production volume of 37 million units, a 5% QoQ increase, reflecting stocking for e-commerce promotions and new product launches. Its market share stood at 12% with production in the fourth quarter anticipated to remain stable.

Vivo (including Vivo and iQoo) ranked fifth with 27 million units produced, up 4% QoQ and capturing a 9% market share. The company’s performance was similarly driven by new product launches and promotional stockings, with fourth-quarter production expected to remain steady.

Finally, Transsion (including TECNO, Infinix, and itel) rebounded from inventory adjustments in the second quarter to produce 25 million units in the third quarter, marketing a 7% QoQ increase and ranking sixth. Fourth-quarter production is expected to prioritise stability to avoid another inventory surplus.

According to TrendForce the market’s attention is turning to AI-powered smartphones thanks to the burgeoning popularity of AI and highlights that these devices must support on-device AI computation capabilities, such as machine learning and generative AI.

AI smartphones are predominantly positioned as flagship models due to the need for advanced processors and memory specifications. AI smartphones are projected to account for 10% to 15% of total production in 2024.