With TSMC increasing investment in US advanced semiconductor manufacturing, bringing the total to $165 billion, and mass production expected to begin after 2030 - if the three newly planned fabs proceed on schedule – the US will dramatically increase its manufacturing capacity.

TSMC first announced plans for its Arizona fab in 2020 as part of a six-fab expansion strategy, aiming to mitigate geopolitical risks. However, escalating trade tensions and tariff issues have forced the company to accelerate its expansion timeline, noted TrendForce.

Since 2018, global trade conflicts and the COVID-19 pandemic have accelerated supply chain fragmentation, with governments worldwide striving to establish more localised semiconductor production.

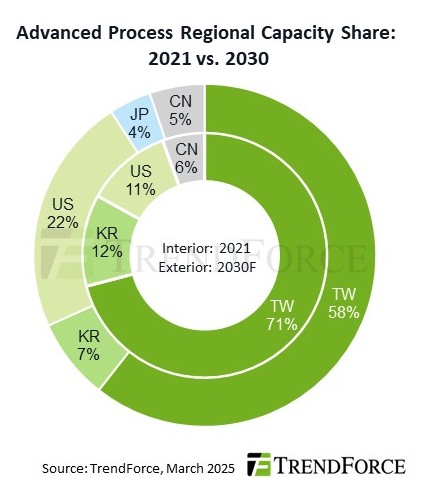

TrendForce data from 2021 indicated that Taiwan accounted for 71% of global advanced node capacity and 53% of mature node capacity. However, by 2030, Taiwan’s advanced process share is expected to decline to 58%, while its mature process share will drop to 30% as the US and China ramp up their semiconductor manufacturing capabilities.

US-based clients represent the largest share of TSMC’s advanced node adoption – hence its decision to ramp up domestic production. TSMC is also establishing two advanced packaging plants and a R&D centre for HPC applications in addition to three new fabs.

Consequently, Arizona is set to become TSMC’s leading overseas technology hub, ensuring comprehensive service for key clients.

While expanding US production reduces concentration risks, it could also lead to higher costs for US IC customers. With higher component and end-product prices there is the potential that consumer purchasing behaviour could be affected.

TrendForce noted that TSMC’s Arizona Phase 1 has just entered mass production, while Phase 2 and Phase 3 are still under construction, with mass production expected between 2026 and 2028.

The actual timeline for the newly announced fabs remains uncertain, with no immediate impact on the industry in the short term. However, in the mid-to-long term, the cost implications and potential price increases across the supply chain will be key factors to watch.